Private Mortgage Insurance is a High-Growth Business

Value Play: NMI Holdings (Nasdaq: NMIH)

The U.S. economy is finally showing signs of “consistently better growth” and a recovery worthy of the name. Since the end of the global financial crisis and recession in 2009, the U.S. economy has only been able to manage sub-par real annual growth in the low-to-mid 2% range through 2014. Last year, annual real GDP rose 2.4%, which was the best result since the end of the 2008-09 recession, but that’s not saying much. But in 2015, US GDP growth is expected to get above the 3% level for the first time since 2005.

One of the main reasons that the overall economic recovery has been so weak is the housing market, which historically has accounted for 17%-18% of the entire economy. Since the 2008-09 recession was caused by the popping of the greatest bubble in home prices in history, it makes sense that recovery from a popped bubble is abnormally slow. Making matters worse was the overly-stringent tightening of mortgage credit in the wake of the housing crisis that retarded recovery.

But the laggard housing market finally appears ready to accelerate in growth and enjoy its time in the sun. New home sales in January were near the fastest pace in more than six years. Bad winter weather in February caused a lull in activity that should prove temporary. National Association of Home Builders Chief Economist David Crowe said in a March 16th statement: “we are expecting solid gains in the housing market this year, buoyed by sustained job growth, low mortgage interest rates and pent-up demand.” Similarly, according to Kiplinger’s most-recent forecast, housing will experience double-digit growth in 2015:

Home builders are looking ahead to a solid year.

We expect single-family housing starts to expand at a double-digit rate in 2015, on a pace to hit 770,000, up from 646,000 last year.

Builders will welcome the increased activity, though the housing sector has much further to grow before reaching 1.15 million units — the number of single-family starts considered typical for a well-functioning housing market.

As for sales of existing homes, we expect them to rebound this year to 5.25 million, from 4.9 million in 2014. New-home sales will reach an average of 520,000 for the year, up 19% from last year.

The reemergence of first-time home buyers, who have largely been sidelined since the recession, will help fuel the housing recovery. The number of first-timers will edge up as a share of all purchasers of existing homes in 2015, from about 28% now to perhaps 30% or a bit above. In good housing years of the past, the share was 35%.

Home prices will continue their upward momentum this year, with growth strongest in the western U.S., where a number of urban areas will approach double-digit gains.

Though mortgage rates will tick up in 2015 along with most other interest rates — to 4.2% from the current rate of 3.8% — they won’t deter most prospective home buyers.

A big reason for the expected resurgence in housing is improved job growth. The February employment report was very strong, showing 295,000 new jobs created. The economy has added more than a million jobs over the past three months, the best 3-month performance since 1997. People are more likely to buy a house if they have a job. As one economist analyzed the situation in late February:

We expect the housing market to improve this year. It is only a matter of time until the improved jobs market has a positive effect on the housing market. We are betting that first-time buyers return this year.

A pickup in housing activity is already happening. On March 12th, the Mortgage Bankers Association (MBA) announced that applications for mortgages to purchase newly constructed homes jumped significantly (up 12%) in February over January. This 12% sequential jump in February was even more impressive given that January applications had also been strong, showing its own year-over-year increase from January 2014. As MBA vice president Lynn Fisher explained: “An increase in mortgage applications to builders in February over strong January numbers bodes well for new home purchases this year.”

NMI Holdings is A Pure Play on the Housing Market

All of this positive macroeconomic data on housing is backdrop to my Front Runner recommendation for the Value Portfolio this month: private mortgage insurer NMI Holdings. One of only seven companies (page 4) in the U.S. to provide private mortgage insurance (PMI), NMI protects mortgage lenders from default-related losses on residential mortgage loans made to home buyers who make down payments of less than 20% of the home’s purchase price. The company went public in November 2013 at an IPO price of $13 per share. With the stock currently trading at only $7.45, new investors can get in at a huge 40% discount.

Two very smart hedge-fund managers have invested in NMI Holdings: Kyle Bass of Hayman Capital (9.4% of shares outstanding) and Howard Marks of Oaktree Capital (4.6% of shares outstanding) and neither has sold any of the shares purchased.

NMI’s business model is unique and gives it a competitive advantage in the PMI market. Most PMI companies get paid to insure mortgages underwritten by others. The problem with this business model is that the PMI company has no control over vetting the borrowers to ensure that they are capable of repaying the loan. The result is distrust, which requires charging higher insurance rates to protect itself from fraud (e.g., liar loans), and a lengthy 36-month waiting period of timely interest payments before the PMI company is willing to waive its rights of rescission (voiding the insurance contract). In contrast, NMI Holdings is the only PMI company to underwrite every mortgage that it insures. Because it has control over vetting, it is very confident in the ability of borrowers to repay the loan and can charge lower insurance rates because the risk of default is lower. Furthermore, it was the first PMI company to reduce the waiting period prior to rescission waiver to only 12 months of timely interest payments because, again, it has confidence in the borrowers it has underwritten.

Unlike all of my other Value recommendations, NMI is not profitable, losing money in each of its quarterly financial periods since its inception. The lack of profitability does not bother me because I know it is just a matter of time before the company grows its book of insurance-in-force to the critical mass necessary to turn a profit. All of the overhead costs necessary to run a business are already in place, whereas the income-producing insurance policies must be built up over time. With infrastructure costs front-loaded and income potential back-loaded, quarterly losses during the current developmental stage of the business cycle are perfectly normal and expected. NMI is classified by Morningstar as “speculative growth” because it is development stage and not profitable yet. The Value Portfolio deserves one speculative company. NMI CFO Jay Sherwood offered the following explanation:

NMI spent much of the time since it opened in 2012 hiring its management team and sales force as well as building the necessary information technology and operational infrastructure. While this building phase was not as exciting as generating revenue from issuing mortgage insurance policies, it was a necessary part of our development and we believe we are now ready to face off with the market.

According to Sherwood, the breakeven point for profitability will occur when the company’s book of insurance-in-force reaches between $12 billion and $14 billion. As of the end of 2014, NMI had $3.37 billion of insurance in force, so it’s only a quarter-way to breakeven. Its growth rate of new insurance written is extremely high, however, so quadrupling its insurance book shouldn’t take long. Take a look at the insurance growth NMI has experienced over the past four quarters:

Tremendous Growth in NMI Holdings’ Insurance-in-Force

Insurance Segment | Dec. 31, 2014 | Sept. 30, 2014 | June 30, 2014 | March 31, 2014 | Dec. 31, 2013 |

New Insurance Written (NIW) | $1.69 billion | $975 million | $430 million | $354 million | $158 million |

Insurance in Force | $3.37 billion | $1.81 billion | $940 million | $515 million | $162 million |

% Growth from Previous Quarter | 93% | 104% | 83% | 218% | N/A |

Source: Company Q4 2014 Report

Between December 2013 and December 2014, NMI’s book of insurance-in-force rose 20-fold ($3.37 billion vs. $162 million). Although continued 20-fold growth is not realistic, a quadruple to breakeven appears easily achievable. A similar development-stage mortgage insurance company called Essent Group (NYSE: ESNT) reached breakeven very quickly, so there is precedent in favor of NMI doing the same. Essent began operations in early 2010 and was unprofitable for its first three years, but hit breakeven in 2013 and has been profitable ever since. Essent ended fiscal 2011 with $3.38 billion of insurance-in-force, which is almost identical to the $3.37 billion of insurance-in-force that NMI has right now. At the end of fiscal 2012, Essent had $13.63 billion of insurance-in-force and $28.20 billion after nine months of fiscal 2013 (page 66). So, yes, NMI should easily be able to break even and generate profitability soon thereafter.

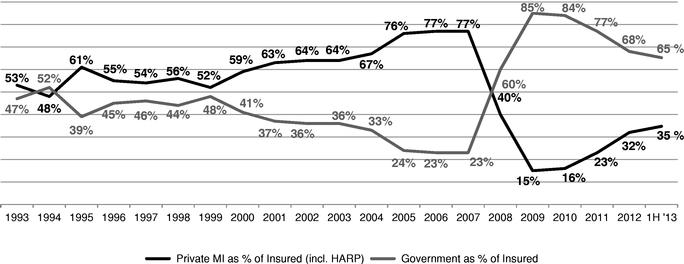

Growth should be easy for NMI because of favorable industry dynamics. About 34% of all mortgage loans are high loan-to-value (i.e., down payments of less than 20% of purchase price), which require mortgage insurance. Prior to the financial crisis of 2008-09, PMI companies were the primary insurance source for low-down-payment home mortgages (i.e., less than 20% equity), representing almost 60 percent of the total in 2000 and 77 percent in 2007. The housing collapse and debt defaults of 2008-09 seriously damaged PMI companies, which either stopped writing new policies or significantly jacked up insurance premiums to compensate for prior losses. The U.S. government picked up the slack through insurance provided by the Federal Housing Administration (FHA) and Veterans Affairs (VA). In 2009, PMI market share had collapsed to only 15% while FHA/VA market share skyrocketed to 85%. Even now six years into an economic recovery, the government’s market share remains abnormally high at 60%-65%, with PMI having risen only to 35%-40%. There is a long way to go until PMI’s market share returns to its normal level of 60-65%. Whereas mortgage loans insured by FHA/VA are sold to Ginnie Mae, mortgage loans insured through PMI are sold to Fannie Mae and Freddie Mac. (see chart on page 4 of NMI Investor Presentation).

{kind=link}

Until very recently, the U.S. government has made a determined effort to reduce public exposure to home-mortgage defaults by increasing the rates it charges for mortgage insurance. Since 2010, when the FHA was charging an annual mortgage insurance premium (MIP) of only 0.55% of the principal amount, the MIP percentage increased all the way up to 1.35% in 2013. At the time of the last MIP increase in January 2013, FHA Commissioner Carol Galante explained that:

These are essential and appropriate measures to manage and protect FHA’s single-family insurance programs. In addition to protecting the MMI Fund, these changes will encourage the return of private capital to the housing market.

Similar sentiment was expressed as recently as this month (March 2015) when Michael Stegman, Treasury Department Counselor to the Secretary for Housing Finance Policy, spoke at the National Council of State Housing Agencies Legislative Conference on the issue of ending government control of Fannie Mae and Freddie Mac and said:

Let me be clear: the Administration stands by our belief that the only way to responsibly end the conservatorship of Fannie Mae and Freddie Mac is through legislation that puts in place a sustainable housing finance system that has private capital at risk ahead of taxpayers, while preserving access to mortgage credit during severe downturns.

In other words, the U.S. government wants private mortgage insurers to succeed because PMI companies further the government’s objective of reducing public exposure to mortgage defaults by shifting mortgage insurance obligations to private risk capital. It always helps when the government is on your side.

The one “fly in the ointment” is that the Obama Administration inexplicably shifted gears this past January and lowered the FHA annual MIP percentage by a whopping 50 basis points from 1.35% to 0.85%. According to Bloomberg, Obama succumbed to the lobbying efforts of realtors who wanted to stimulate more home sales by making it less costly for lower-income, first-time homebuyers to obtain a mortgage. Republicans in Congress criticized Obama’s decision to cut premiums. Tennessee Senator Bob Corker, who sits on the Senate Banking Committee, said it was “bad news for taxpayers” and “yet another irresponsible, head-scratching decision from the administration in regards to our nation’s housing finance system.”

The stocks of all PMI companies fell on the news of the FHA premium cut, including NMI. Nevertheless, the stock sell-off was overdone given the limited negative impact of the rate cut on competition. In the February conference call, NMI CEO Brad Shuster explained that the FHA price drop would only affect “less than 10%” of the company’s loan volume and consequently he was not worried:

Now turning to the competitive environment. The most notable recent change is the 50 basis point premium rate reduction by the FHA. As many of you know, the FHA been raising mortgage insurance premiums over the past several years and we believe those increases have contributed to a share again for private mortgage insurers over that time frame. However we believe that many factors influence lenders and borrowers when it comes to the decision to go FHA or conventional, including the nonrefundable upfront mortgage insurance premium charged by the FHA, the ease and speed of underwriting and the preferences of market participants.

Also although the price change mathematically reduces our price advantage on around 20% of our production, the monthly payment spread on an average loan is less than $20 for the majority of that production. Given this small spread on pricing and the other factors I previously mentioned, we believe that less than 10% of our production could be sensitive to the price change. Our experience has been that lenders are measured in their reactions to these price changes.

In addition, the government-sponsored entities (GSEs) could reduce GSEs’ loan-level pricing adjustments (LLPAs) following the release of the final PMI eligibility requirements by mid-year. This could potentially reduce the FHA pricing advantage in certain risk categories and lenders may wait to see how these events unfold. This leads us to believe that the FHA reduction will not have a significant impact on the 2015 production.

LLPAs are surcharges that the GSEs (Fannie Mae and Freddie Mac) currently impose on mortgage originators that want to sell their mortgage loans made to borrowers with low credit scores. Mortgage originators must pass through these LLPAs to the borrower, which increases the effective rate of the loan. If the LLPAs were reduced, the loan rate available to borrowers with low credit scores would be more competitive with the FHA-backed mortgage loans and more borrowers would opt for mortgage loans underwritten with PMI instead of an FHA loan. Given that the Obama Administration is willing to jeopardize the financial strength of FHA/VA through the premium reduction, it may also be willing to jeopardize the financial strength of Fannie Mae and Freddie Mac by reducing LLPAs, which would level the playing field and help the PMI companies.

Furthermore, the greatest effect of the FHA premium cut would be on mortgages underwritten for borrowers with the lowest credit quality, which is the riskiest and least-attractive segment for PMI companies anyway. As two analysts pointed out:

- Susquehanna: FHA premium cut is “largely immaterial” to PMI company earnings. Even with the annual premium cut, FHA charges an additional up-front mortgage insurance premium that remains much higher than the LLPAs and adverse market delivery charges (AMDCs) that Fannie and Freddie charge on PMI mortgage loans at higher credit-quality levels.

- FBR: PMI companies are largely insulated from FHA premium cut, which focuses on low-quality borrowers, because PMI companies focus on higher-quality borrowers where PMI is still “a better deal.” Reduced LLPAs are also likely and would make PMI even more competitive. Pre-housing bubble (i.e., before 2008), PMI companies charged higher insurance premiums than FHA and yet stilled garnered significantly more market share thanks to private sector’s ability to underwrite loans more quickly.

{kind=link}

The Federal Housing Finance Agency (FHFA) has proposed new private mortgage insurer eligibility requirements (PMIERs) that are expected to be finalized in mid-2015. NMI has filed its comments on the proposed rules and the hope is that the rules limit eligibility to companies with strong balance sheets like NMI so that the number of PMIs does not expand much beyond the current seven companies. Reduced LLPAs may also be part of the new rules.

Valuation is another consideration and NMI Holdings is trading at a much-cheaper multiple of price-to-book value than other PMI companies. Given that NMI is development stage and is not yet generating positive earnings, a price-to-book-value ratio is the appropriate valuation measure for insurance companies. The median price-to-book-value ratio of PMI companies is currently around 3.2 times and has historically averaged around 2.5 times (see Page 5 of NMI investor presentation). In contrast, NMI Holdings is trading at only 1.03 times book value! That is super cheap on a relative basis and suggests that the stock could easily double or more in price once it reaches profitability. Furthermore, the balance sheet is strong with zero debt.

NMI’s cheap valuation not only explains why Kyle Bass and Howard Marks continue to hold on to their shares, but it also explains why the stock has seen a recent surge in insider buying by two directors and the general counsel.

Bottom line: NMI Holdings has tremendous growth potential in an improving mortgage market. It’s strong balance sheet and competitive advantage in low-cost self-underwriting makes it a strong buy at its current cheap valuation.

NMI Holdings is a buy up to $10; I’m also adding the stock to my Value Portfolio.

Value Sell Alert

To make room for NMI Holdings, Roadrunner is selling:

- AGCO Corp. (AGCO)

Although my long-term bullishness on this agricultural equipment manufacturer remains intact, the fact remains that reduced farm income makes it likely that earnings and revenues for AGCO may not experience a trough until 2016, so the timeliness for a sustained up-move in the stock price is lacking and an investment may be dead money for up to 12-18 months. Given that the Value Portfolio has a limit of 20 holdings, AGCO must be sacrificed — for now — to make room for a stock with a more near-term catalyst for price appreciation.

AGCO Corp. is being sold from the Value Portfolio.

Momentum Buy:

Super Micro Computer (Nasdaq: SMCI)

Super Micro Computer is a global leader in high-performance, high-efficiency server technology and innovation is a premier provider of end-to-end green computing solutions.

System solutions cover a broad range of applications across data center and cloud services, large scalable server farms, scientific and research supercomputing clusters, businesses with complex computing requirements (such as those in financial services, oil and gas exploration, and media and entertainment companies), medical equipment and digital security and surveillance. Founded in 1993 and headquartered in San Jose, California, Supermicro has been profitable every year since its inception. Analyst earnings estimates are rising, which is a good sign and suggests that Super Micro Computer may be “an impressive growth stock.”

- Price gain between 12 months ago and 3 months ago = 90.18% (100th percentile)

- Price gain over the past 2 months =-3.76%

- Price gain over the past month = -8.43%

- Roadrunner Momentum Rating: 90.18 – (3.76) – (3*-8.43) = 111.71

Super Micro Computer is a buy up to $41.00; I’m also adding the stock to my Momentum Portfolio.

Momentum Sell Alert

To make room for the new momentum stock, Roadrunner will be selling the following price laggard:

- Bitauto Holdings (BITA)

The economic slowdown in China is hurting Internet advertising which is the main source of revenue and income for automobile information websites like Bitauto. I sold Autohome last month based on this economic slowdown and obviously should have sold Bitauto at the same time for the same reason. Better late than never.

Stock Talk

Add New Comments

You must be logged in to post to Stock Talk OR create an account