Full Hearts, Thin Yields

The joint monthly web chat for subscribers of The Energy Strategist (TES) and MLP Profits (MLPP) took place two weeks ago. The chat is conducted by Igor Greenwald, who is managing editor for TES and chief investment strategist for MLPP, and myself on the second Tuesday of each month.

We had quite a busy session, and had a few questions remaining at the end. Some required an extended answer, or a bit more research. The remaining questions that were MLP-focused will be answered here, while more generally themed energy questions are answered in this week’s Energy Letter.

Q: Do you see the market price acceleration for the high growth MLPs continuing?

Igor and I both addressed questions related to this theme in the chat, but I want to elaborate here. We both feel like some MLPs have risen too far, too fast, and have been advising subscribers to lighten up on certain MLP holdings. I have been astounded by the performance of certain MLPs, and believe some of them now belong only in the most aggressive portfolios. At a minimum many are unsuitable for risk-averse investors, or typical income-seeking MLP investors.

MLPs that specialize in sand for hydraulic fracturing, like Hi-Crush Partners (NYSE: HCLP) and Emerge Energy Services (NYSE: EMES), have shown outstanding performance since their IPOs, but if there is any slowdown in business each could be in for a sharp correction.

Likewise, Phillips 66 Partners (NYSE: PSXP) has risen 154% since its IPO just under a year ago, pushing the yield down to 1.45%. So why do investors keep bidding the price higher with the yield so low? Because they have very aggressive expectations of how the partnership will grow its distribution. Anything that falls short of those aggressive expectations could result in a sharp pullback in the unit price.

Q: How do you project that the recent announcement about EPD being able to ship overseas affect the price?

The question relates to the recent announcement that the US Department of Commerce’s Bureau of Industry and Security issued private rulings allowing Pioneer Natural Resources (NYSE: PXD) and Enterprise Products Partners (NYSE: EPD) to export minimally processed condensate from natural gas fields. This condensate had been subject to the US ban on crude oil exports, but the ruling has now classified minimally processed condensate as a refined product, and therefore eligible for export. The US Gulf Coast has had a glut of condensate, since most refineries in that area are more geared toward processing heavier oil, and as a result condensate prices have been depressed.

In the near-term, this ruling won’t have a huge impact on EPD’s bottom line. The amounts that will be exported are reportedly small. EPD’s unit price began to move higher in the days leading up to the announcement, and is up about 5% in the past two weeks. But we still like Enterprise as one of the most attractive and most conservatively managed MLPs.

Q: What are your thoughts about the strength of NuStar Energy and how does it stack up against other MLPs?

NuStar Energy (NYSE: NS) is one of the smaller midstream partnerships with a market capitalization of $5.1 billion. The partnership has operations in the US, Canada, Mexico, the Netherlands, the Caribbean, the UK and Turkey. After selling off a 50% interest in an asphalt venture earlier in the year, Nustar operates in three segments: Storage, Transportation, and Fuels Marketing.

Nustar’s storage division owns terminal and storage facilities for petroleum products, specialty chemicals, crude oil, and other feedstocks; and crude oil storage tanks. Nustar has 84 terminal and storage facilities that store and distribute crude oil, refined products and specialty liquids. The partnership has approximately 92 million barrels of storage capacity

The transportation segment transports refined petroleum products, crude oil, and anhydrous ammonia across more than 8,600 miles of pipeline, mostly in the Midwest.

The fuels marketing segment purchases crude oil, fuel oil, bunker fuel and other refined products for resale. Crude and refined product customers include major integrated refiners and trading companies. Bunker fuel customers are mainly ship owners, including cruise line companies.

Nustar has performed well over the past 12 months, with a total return of 53.4% and a year-to-date total return of 32.3%. Nevertheless, the yield is still attractive at 6.7% annualized based on the most recent distribution.

On the downside, the partnership hasn’t grown its distribution since 2011, and the coverage ratio for the past 12 months is low at 0.83x. However, there was improvement in the coverage ratio in each of the past four quarters, with the most recent two quarters having coverage ratios of 0.90x (2013 Q4) and 0.93x (2014 Q1).

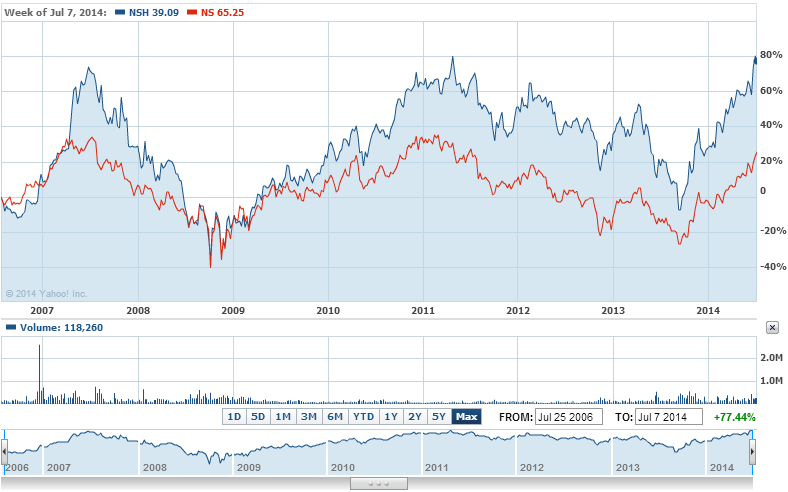

NuStar Energy does have a publicly traded general partner in NuStar GP Holdings (NYSE: NSH) which went public in 2006. The GP pays a lower dividend at 5.8 percent, but has significantly outperformed the limited partner since it went public:

NuStar pays a higher dividend than most of its larger competitors, and after three years of disappointing returns its fortunes look to be on the upswing now that it’s divested its money-losing asphalt business. This is definitely one worth considering for your portfolio.

Q: Do you follow any of the energy trusts such as Pacific Coast Oil Trust and VOC Energy Trust? The distributions are generous. ROYT is near its 52 week low. Any thoughts on either of these?

We do follow them, but generally don’t like the risk/reward ratio for most MLP investors. I have had some conversations with investors who were chasing the 12-14% yields on these trusts without really appreciating the underlying risks. As you note, Pacific Coast Oil Trust (NYSE: ROYT) is near its 52-week low after declining by 25% over the past year. Those high yields provide little consolation given that sort of downside risk.

Q: Please share your thoughts on Holly Energy Partners and Atlas Pipeline Partners.

The refinery logistics segment has done quite well, even when the associated refiner has struggled a bit. We like Holly Energy Partners (NYSE: HEP) for the long haul. I covered the partnership in some depth in Holy Holly, What a Deal.

Like NuStar, Atlas Pipeline Partners (NYSE: APL) is a smallish ($2.7 billion market capitalization) midstream operator with a bigger yield (7.3% annualized) than its larger competitors. Atlas offers gas gathering, compression, processing and treating services and owns and/or operates 11,200 miles of natural gas gathering systems in Oklahoma, Kansas and Texas — plus another 100 miles of natural gas gathering systems in Tennessee.

The partnership hasn’t performed well over the past year, with a 12-month total return of -8.3%. Nevertheless, its coverage ratio over the past year has been a healthy 1.02x, and it grew the distribution by nearly 8% in the past year. Despite questions about recent growth, this one certainly has some upside potential.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

China Calling LNG Play

The future may be bright for the global trade in liquefied natural gas (LNG) but its present is characterised by too many ships and not enough super-cooled gas to haul to Asia and Europe. Delays on Australian export projects and the long lead time ahead of the expected ramp in US exports later in the decade have pushed LNG charter rates sharply lower from their peak a couple of years ago.

In these circumstances, having a fleet almost fully chartered for the next three years is a huge plus, and that’s the winning proposition offered by Teekay LNG Partners (NYSE: TGP). The unit price has lagged the gains by other LNG fleet operators over the past year, but has been making up some ground of late as investors warm to TGP’s 6% yield and secure distribution.

Sentiment has been boosted by the recent announcement of a deal to take partial stakes in four BG Group (London: BG, OTC: BRGXF) LNG carriers currently under construction in China, which are scheduled to enter service under 20-year extendable charters between 2017 and 2019. TGP has also entered into a 50/50 venture with a closely held Chinese firm to build six icebreaker LNG carriers that will serve Yamal LNG, an export terminal planned for northern Russia.

Both deals enhance TGP’s long-term revenue outlook while allowing it to make further inroads in China, which is expected to become the leading LNG shipping market.’

The unit price hit a record two weeks ago and looks poised to continue higher. Buy TGP below the newly increased limit of $52.

— Igor Greenwald

Stock Talk

ChesapeakeHolding

Is the reason for the drop in the price of ROYT because the distribution has dropped from the initial rates? The distribution seems to be stabilizing in the 12-14 cent per month range. At the current price of $12.60 to $13.00, what is the big risk? The 11% yield is generous I know, but as long as the distribution stays in the 12-14 cent range what is the potential downside risk to the stock price? I have a small position (1900 shares) that I am in at $12.75. I am treating it as a bond with a nice yield and with a potential 8% downside. Are my thoughts reasonable or am I in outer space.

Thank you.

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account