Commercial Construction Materials and Orthopedic Implants

Momentum Play: Apogee Enterprises (Nasdaq: APOG)

As I wrote in my Frontrunner recommendation of Stewart Information Services in the September issue of Roadrunner Stocks, the U.S. housing market has entered a sustained recovery. The Federal Reserve’s October 30th policy statement notes that residential housing has temporarily cooled in reaction to higher interest rates, but it will prove the pause that refreshes.

What is less well known than the strong recovery in residential housing is the slow-but-sure comeback in non-residential construction. According to Anirban Basu, chief economist for Associated Builders and Contractors, nonresidential construction is roughly nine months behind the residential-construction recovery. So, if you feel that you’ve missed out on making the easy profits – the low-hanging fruit—from the housing recovery, investing in non-residential construction may give you a second chance to win big.

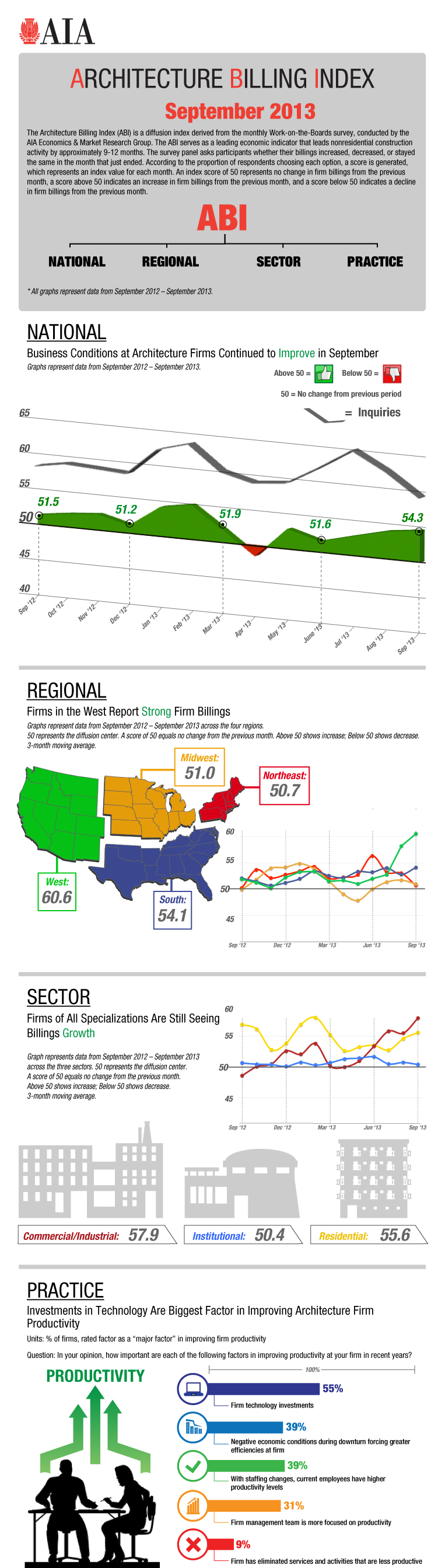

A leading indicator for non-residential construction is the Architecture Billings Index (ABI). Real-estate developers need to pay architects for designs before they can actually start construction. According to the American Institute of Architects, the ABI “reflects the approximate nine-to-twelve-month lead time between architecture billings and construction spending.” In September, the ABI hit 54.3, which is the highest reading in seven months (February 2013 saw 54.9) and the 13th time in the past 14 months that the index has increased. Any number above 50 signifies growth, so it’s a good time to be an architect!

{kind=link}

The FMI Nonresidential Construction Index (NCRI) has also been on the rise. At the end of the third-quarter, the index was at an expansionary 60.3 – the highest reading since the inception of the NCRI in 2007 (i.e., six years ago). With the ABI currently at a near-peak reading, there is reason to believe that the NCRI will play catch-up and continue its upswing into the future.

To play the impending upswing, I’ve chosen Minnesota-based Apogee Enterprises. The company operates in four business segments:

|

Business Segment |

Operating Profit Margin |

Percent of Total Sales |

Market Share |

|

Architectural Glass |

-1.6% |

36.8% |

70.0% |

|

Architectural Framing Systems (aluminum) |

7.6% |

26.4% |

10.0% |

|

Architectural Services (installation) |

-0.5% |

25.8% |

7.5% |

|

Large-Scale Optical |

26.3% |

11.0% |

75.0% |

Source: Company website

The takeaway from the above table is that the company’s largest segment (architectural glass) is losing money and its smallest segment (large-scale optical, which involves value-added picture framing) is making the most money. Not ideal, but the silver lining is that there is much room for improvement. At their last business-cycle peaks, the architectural glass segment achieved a 9.1% operating margin in 2007-08 and the architectural services segment achieved a 9.0% margin in 2009-10. Right now, Apogee’s total revenues are $728 million and its overall operating profit margin is only 4.5%, but the company’s three-year target (mid-2015) is $1 billion in revenue and a 10% operating margin, which would more than double profits. Part of the current margin problem is simply a timing issue, with customers delaying — not canceling – scheduled projects, but the macroeconomic environment for non-residential construction market has not yet moved into a strong uptrend. A strong uptrend is coming, however, as CFO James Porter stated in a Sept. 19th conference call:

We’ve maintained our outlook for high-single-digit top line growth despite limited help from domestic commercial construction markets. We have a nice backlog level and are seeing very good bidding activity. In our longer lead time projects-driven businesses, though, the majority of work that will be coming in as bookings is going to generate revenues for fiscal 2015 and beyond.

The external metrics we watch, including job growth, the Architectural Billings Index, the McGraw-Hill Construction forecast and consumer confidence continue to point to improving markets for Apogee, consistent with what we see with our bidding activity. Our second half is then expected to be stronger than the first half. We should see nice top line sequential growth from the second quarter.

Second-quarter financials saw flat revenue (up 1%) but strong earnings growth (17%) as the company focuses on efficiency improvement while it waits for the macroeconomic rebound. Apogee is cutting costs and getting “lean and mean,” so its operating leverage will maximize profit growth when the industry upturn occurs. CEO Joseph Puishys currently characterizes U.S. commercial construction as “modest” but is confident that Apogee can “outperform domestic commercial construction market growth by several percentage points.”

In commenting on Apogee’s second-quarter report, Zacks was optimistic about the future:

Apogee’s backlog remains strong, which bodes well for its future performance. Apogee has faced challenging commercial construction market conditions so far. However, U.S. construction is finally stabilizing and is on track to the much-awaited recovery, which looks promising for Apogee.

Equally sanguine is Goldman Sachs, which on October 1st added Apogee to its buy-rated Conviction List, stating:

Shares of APOG are poised to benefit over the medium-term alongside a recovery in nonresidential construction. We view the company’s improving cost structure and emphasis on profitable growth as accelerants of this exposure and expect incremental margin to benefit materially. Further, we note APOG has attractive portfolio diversification characteristics. The Large-Scale Optical segment (53% of EBIT) provides ballast to earnings and cash flow, and has exhibited consistent performance over a 10-year period.

Apogee is not much of a growth stock; it is more of a cyclical stock. Revenue and earnings have negative growth rates over the past five and ten year-periods. The company is trying to expand its geographic reach beyond North America. It owns a glass fabricator in Brazil and is successfully exporting its custom framing business to European museums (slide no. 9). For the most part, however, Apogee is a U.S.-centric company and the investment play here is on six-sigma efficiency improvements and a cyclical upturn in the U.S. non-residential construction industry. Looking at the company’s historical returns on equity and earnings per share, one can see the potential for a much-higher valuation once the cycle turns up:

|

Fiscal Year |

Return on Equity |

Earnings Per Share |

|

Trailing 12 Months |

6.87% |

$0.78 |

|

2013 |

5.84% |

$0.67 |

|

2012 |

1.43% |

$0.17 |

|

2011 |

-3.08% |

-$0.37 |

|

2010 |

9.62% |

$1.15 |

|

2009 |

16.98% |

$1.81 |

|

2008 |

18.66% |

$1.67 |

As you can see, the company’s financials have recovered somewhat from the fiscal 2011 bottom, but they have a ways to go to get back to the peak profitability of fiscal 2008 and 2009. When Apogee gets back to these peak figures, the stock price could rise substantially. Keep in mind that Apogee’s cyclicality means that investors will probably lower the earnings multiple afforded the stock near its peak earnings, so one shouldn’t assume if its earnings rise 132% from $0.78 to $1.81 that the stock will rise by the same percentage. But with the stock trading at all-time highs this month despite its earnings being less than half the prior peak, investors are exhibiting confidence that the prior peak will be reached and perhaps surpassed.

Apogee’s valuation is not cheap from a historical perspective, but the stock’s momentum is strong and its current EV-to-EBITDA ratio of 14.32 is not exorbitantly high. I like the company’s Midwestern corporate culture, which stresses ethical values and its CEO Joe Puishys has more than 30 years manufacturing experience, mostly with Honeywell. The debt-to-capital ratio is very low at less than 10%.

Bottom line: Apogee is a strong momentum stock with improving financials, market-leading positions, and operates in an industry (non-residential construction) that is on the verge of a long-lasting cyclical uptrend.

Apogee Enterprises is a buy up to $37; I’m also adding the stock to my Momentum Portfolio.

Value Play: Exactech (Nasdaq: EXAC)

Orthopedic surgery and implant stocks are hot! On September 25th, Stryker Corp. (NYSE: SYK) agreed to acquire MAKO Surgical (Nasdaq: MAKO) for $1.65 billion in cash. The buyout price represented a huge 89-percent premium to the 20-day moving average of MAKO’s stock price. To put this into perspective, the deal is the second-highest premium ever paid for a medical-products company worth more than $500 million. Millennium Research Group forecasts “strong growth in all segments of the orthopedic extremity device market” through 2021. Extremity devices are orthopedic implants other than hips, knees, and spines. Examples include shoulders, wrists, elbows, fingers and toes, and ankles.

By 2016, the extremity implant market should total $4.2 billion. By contrast, total sales of orthopedic devices reached $43.1 billion in 2012. This strong growth in extremity devices will make it economically attractive for large medical device companies to buy the successful technology of smaller companies rather than try to develop the technology itself. According to Millennium:

Merger and acquisition activity will continue to be a prominent feature in this space. Larger companies are better positioned to cross-sell products attained through the acquisition of smaller companies. In turn, products developed by smaller companies tend to cater to niche markets, offering an attractive means for large companies to supplement their product portfolios.

Wall Street analysts believe the MAKO acquisition is just the beginning of an industry-wide consolidation. According to Joanne Wuensch of BMO Capital Markets:

The deal is likely to signal the start of additional industry consolidation. We anticipate that the transaction will drive the other M&A medtech targets’ stock prices higher, as the musical chairs move in consolidation has begun.

Similarly, Matt Miksic of Piper Jaffray said:

The appetite is out there. From the target side, there are some in the growthier, more attractive medical-device markets.

Lastly, Mike Matson of Needham & Co. stated:

Large medical-technology companies are likely seeking targets with commercialized products, differentiated technologies, and higher revenue growth that operate in attractive markets adjacent to their own.

Increased global demand for orthopedic implants is a direct result of the mega-trend toward an older population and the inevitable joint deterioration that takes place with aging:

Patient and surgeon demand for extremity procedures continues to grow, fueled by the rise in the over-50 population, the increasingly active aging population and the growing number of sports injuries in the younger population. Rising rates of obesity, osteoarthritis and osteoporosis also contribute to injuries to the extremities that require surgical treatment. Increased marketing by manufacturers has raised awareness of available treatments, further fueling procedure growth.

According to a 2012 report by Orthoworld (page 2), the segment of the population over the age of 45 is growing 3% annually, triple the rate of 1% for the overall population. Furthermore, 97% of all joint replacement procedures are performed on patients over the age of 45. The report suggests that demographics alone will drive growth in global orthopedic sales.

Analysts are speculating that Wright Medical Group (Nasdaq: WMGI) might be the next takeover target because of its higher-than-average growth rate, but there is another orthopedic device company expected to grow even faster than Wright and is priced at much lower valuation multiples: Exactech (Nasdaq: EXAC).

Exactech is Growing Fastest and Priced Cheapest!

|

Company |

EV-to-EBITDA Ratio |

P/E Ratio |

Est. 5-Year Annual Earnings Growth |

PEG Ratio |

|

Exactech |

8.37 |

19.93 |

14.00% |

1.42 |

|

Johnson & Johnson (JNJ) |

11.00 |

20.81 |

6.27% |

2.70 |

|

Smith & Nephew plc (SNN) |

10.28 |

21.17 |

7.85% |

2.03 |

|

Sykes Enterprises (SYK) |

15.70 |

31.74 |

8.16% |

2.14 |

|

Wright Medical Group |

26.34 |

115.47 |

13.50% |

-3.69 |

|

Zimmer Holdings (ZMH) |

9.34 |

22.21 |

9.25% |

1.67 |

Source: Bloomberg

Exactech was founded in 1985 by orthopedic surgeon Bill Petty, who at the time was Chairman of the Department of Orthopedic Surgery at the University of Florida’s medical school. He believed that orthopedic surgeons would appreciate orthopedic implants designed by a fellow orthopedic surgeon. Exactech’s strong growth since its founding is proof Dr. Petty was right. Annual sales have grown 120-fold since 1990 (slide no. 4) – from $2 million to $239 million. Over the past 10 years, revenue has grown at an annualized double-digit rate of 14.2% and earnings have grown at a 7.18% clip. Earnings growth appears to be accelerating, with the most-recent third-quarter financials showing a 21.1% growth rate.

The company has five operating segments, each of which grew both net income and cash flow in the just-completed third quarter:

|

Business Segment |

Percent of Total Sales |

Annual Growth Rate (2011-12) |

|

Knee |

36.3% |

3.1% |

|

Extremities |

23.2% |

31.3% |

|

Hip |

10.9% |

22.1% |

|

Biologics and Spine |

26.3% |

1.6% |

|

Other (e.g., bone cement) |

11.4% |

-4.5% |

Source: Company 10-K Filing (p. 28)

As the table above demonstrates, Exactech is focused heavily on extremity devices, which are the industry’s fastest-growing segment. This fact explains why the company is forecast to grow much faster than the industry and why it could be a takeover target. Its market capitalization is only $306 million, which would be easily affordable to any would-be acquirer – less than one-fifth the $1.65 billion Stryker paid for MAKO.

Other aspects of Exactech that I like are its low debt level, high insider ownership, and founder CEO. The debt-to-capital ratio is a very-reasonable 19.38% and insider ownership stands at 33.6%. CEO and co-founder Bill Petty loves his company and is focused on its long-term success. When Dr. Petty retires (he is 70 years of age, after all!), the company will remain in the founding family since his son David is Exactech’s president.

Exactech is a buy up to $26; I’m also adding the stock to my Value Portfolio.

Stock Talk

Add New Comments

You must be logged in to post to Stock Talk OR create an account